# dYdX Documentation

import { HomePage } from 'vocs/components'

dYdX DocumentationThis website contains all the required documentation for dYdX protocol to start trading.Get startedGitHub

## Open Source Repositories

Please find the open source repositories on our [GitHub](https://github.com/dydxprotocol):

* [Monorepo](https://github.com/dydxprotocol/v4-chain)

* [Protocol](https://github.com/dydxprotocol/v4-chain/tree/main/protocol)

* [Indexer](https://github.com/dydxprotocol/v4-chain/tree/main/indexer)

* [Clients](https://github.com/dydxprotocol/v4-clients)

* [Frontend](https://github.com/dydxprotocol/v4-web)

* [iOS](https://github.com/dydxprotocol/v4-native-ios)

* [Android](https://github.com/dydxprotocol/v4-native-android)

* [Terraform](https://github.com/dydxprotocol/v4-infrastructure)

* [dYdX Technical Docs](https://github.com/dydxprotocol/v4-documentation)

* [Pocket protector TG bot docs](https://docs.pocketprotector.xyz/)

When contributing, please ensure your commits are verified. You can follow these steps to do so:

* [Generate a new signing key](https://docs.github.com/en/authentication/managing-commit-signature-verification/generating-a-new-gpg-key) for work use and [turn on Vigilant Mode](https://docs.github.com/en/authentication/managing-commit-signature-verification/displaying-verification-statuses-for-all-of-your-commits)

* [Tell Git about your GPG key](https://docs.github.com/en/authentication/managing-commit-signature-verification/telling-git-about-your-signing-key) and install `pinentry` if necessary

#### Third-Party Integrations

* [LEAN / dYdX Exchange Plugin](https://qnt.co/dydx-lean-repo)

## Third-Party Integrations

### QuantConnect

QuantConnect is a leading algorithmic trading platform that empowers developers and traders to research, backtest, and deploy quantitative strategies across various asset classes. The [integration with dYdX](https://qnt.co/dydx-docs) enables members to live trade Crypto Futures on the dYdX decentralized exchange from within the QuantConnect platform. QC's battle-tested infrastructure provides a stable environment that handles all the communication with the dYdX API, so you can focus on researching new strategies and monitoring your live algorithms. The LEAN engine that powers QC has an extensive suite of features to equip you with all the AI models, indicators, and dataset you'll need to take your trading to the next level with just a few lines of code.

## TODO

#### Fill

Add testnet USDC to a subaccount.

##### Method Declaration

:::code-group

```python [Python]

async def fill(

self,

address: str,

subaccount_number: int,

amount: float,

headers: Optional[Dict] = None,

) -> httpx.Response

```

```rust [Rust]

pub async fn fill(&self, subaccount: &Subaccount, amount: &Usdc) -> Result<(), Error>

```

```typescript [TypeScript]

public async fill(

address: string,

subaccountNumber: number,

amount: number,

headers?: {},

): Promise

```

```url [API]

/faucet/tokens

```

:::

##### Parameters

| Parameter | Location | Type | Required | Description |

| ------------------- | -------- | ------------------ | -------- | ------------------------------------------------------------ |

| `address` | body | [Address] | true | The wallet address that owns the account. |

| `subaccount_number` | body | [SubaccountNumber] | true | A number that identifies a certain subaccount of the address |

| `amount` | body | [BigDecimal] | true | Amount to fill |

##### Response

| Status | Meaning | Schema | Description |

| ------ | ------------- | ------ | ------------------------------------ |

| `200` | [OK] | | The response |

| `400` | [Bad Request] | | The request was malformed or invalid |

| `404` | [Not Found] | | The subaccount was not found. |

[Python] | [TypeScript]

[Python]: https://github.com/dydxprotocol/v4-clients/blob/main/v4-client-py-v2/examples/faucet_endpoint.py

[TypeScript]: https://github.com/dydxprotocol/v4-clients/blob/main/v4-client-js/examples/faucet_endpoint.ts

[Address]: /types/address

[SubaccountNumber]: /types/subaccount_number

[BigDecimal]: /types/big_decimal

[OK]: /types/ok

[Bad Request]: /types/bad-request

[Not Found]: /types/not-found

#### Fill Native

Add native dYdX testnet token to an address.

##### Method Declaration

:::code-group

```python [Python]

async def fill_native(

self,

address: str,

headers: Optional[Dict] = None,

) -> httpx.Response

```

```rust [Rust]

pub async fn fill_native(&self, address: &Address) -> Result<(), Error>

```

```typescript [TypeScript]

public async fillNative(address: string, headers?: {}): Promise

```

```url [API]

/faucet/native-token

```

:::

##### Parameters

| Parameter | Location | Type | Required | Description |

| --------- | -------- | --------- | -------- | ----------------------------------------- |

| `address` | body | [Address] | true | The wallet address that owns the account. |

##### Response

| Status | Meaning | Schema | Description |

| ------ | ------------- | ------ | ------------------------------------ |

| `200` | [OK] | | The response |

| `400` | [Bad Request] | | The request was malformed or invalid |

Examples: [Python]

[Python]: https://github.com/dydxprotocol/v4-clients/blob/3e8c7e1b960291b7ef273962d374d9934a5c4d33/v4-client-py-v2/examples/fund_account_example.py#L25

[Address]: /types/address

[OK]: /types/ok

[Bad Request]: /types/bad-request

import FaucetClient from './intro.mdx'

import Fill from './fill.mdx'

import FillNative from './fill_native.mdx'

## Faucet API

### Methods

## Indexer API

The Indexer is a high-availability system designed to provide structured data. It serves both over its [HTTP/REST API](/indexer-client/http) for spontaneous requests and over its [WebSockets API](/indexer-client/websockets) for continuous data streaming.

See the [guide](/interaction/endpoints#indexer-client) on how to use the available Indexer client to learn how to connect to it.

## Connecting to dYdX

dYdX provides two networks for trading: a **mainnet**, and a **testnet**:

* **mainnet**: The core network where real financial transactions occur;

* **testnet**: A separate, risk-free, network. Served mainly for the purposes of testing and experimenting before transitioning to the **mainnet**.

For the purposes of this guide, we'll assume that the **mainnet** is being used. Nevertheless, the API is exactly the same for both the **mainnet** and the **testnet**, so any code working in the **mainnet** should work in the **testnet**. Choosing between the **mainnet** and the **testnet** is simply a matter of changing the used endpoints.

:::note

It is advisable that for the purposes of learning and trying out the dYdX ecosystem that the **testnet** is used and preferred over the **mainnet**.

:::

### Available clients

Interacting with the dYdX network API is made through several sets of methods grouped with structures referred to as clients. Each of these clients essentially connects to a different server with its own functionality and purpose.

#### Node client

The Node client (also known as the Validator client) is the main client for interacting with the dYdX network. It provides the [Node API](/node-client/index) allowing the user to do operations that require authentication (e.g., issue trading orders) through the [Private API](/node-client/private/index).

You'll need an endpoint to setup the Node client. Grab an RPC/gRPC endpoint from [here](#node). Additionally for the Python client, you'all also need a HTTP and WebSockets endpoints.

:::tip[OEGS]

With the release of the Order Entry Gateway Service (OEGS), users can now connect to dYdX via OEGS endpoints. OEGS provides both gRPC and RPC endpoints.

for more info on OEGS, check [here](/concepts/architecture/oegs.mdx)

:::

:::code-group

```python [Python]

from dydx_v4_client.network import make_mainnet

from dydx_v4_client.node.client import NodeClient

config = make_mainnet( # [!code focus]

node_url="oegs.dydx.trade:443" # [!code focus]

rest_indexer="https://indexer.dydx.trade", # [!code focus]

websocket_indexer="wss://indexer.dydx.trade/v4/ws", # [!code focus]

).node # [!code focus]

# Call make_testnet() to use the testnet instead. # [!code focus]

# Connect to the network. # [!code focus]

node = await NodeClient.connect(config) # [!code focus]

```

```typescript [TypeScript]

import { ValidatorClient, Network } from '@dydxprotocol/v4-client-js';

// Using a pre-configured endpoint. // [!code focus]

const config = Network.mainnet().validatorConfig; // [!code focus]

// Or use `Network.testnet()` for the testnet. [!code focus]

// You can modify the endpoint doing `config.restEndpoint = "...";`

// Connect to the network. // [!code focus]

const node = await ValidatorClient.connect(config); // [!code focus]

```

```rust [Rust]

use dydx::{config::ClientConfig, node::NodeClient};

// The configuration file should have the endpoint. Use a gRPC endpoint. // [!code focus]

let config = ClientConfig::from_file("config.toml").await?; // [!code focus]

// Connect to the network. // [!code focus]

let node = NodeClient::connect(config.node).await?; // [!code focus]

```

:::

While the Node client can also query data through the [Public API](/node-client/public/index), the Indexer client should be preferred.

#### Indexer client

The Indexer is a high-availability system designed to provide structured data and offload computational burden from the core full nodes. The Indexer client provides methods from the [Indexer API](/indexer-client/index). It serves both as a spontaneuous source of data retrieval through its REST endpoint, or a continuous feed of trading data through its WebSockets endpoint.

Given that the Indexer client can use these two different protocols, you'll need two endpoints to setup it up. Grab these from [here](#indexer).

:::code-group

```python [Python]

from dydx_v4_client.network import make_mainnet

from dydx_v4_client.indexer.rest.indexer_client import IndexerClient

from dydx_v4_client.indexer.socket.websocket import IndexerSocket

config = make_mainnet( # [!code focus]

node_url="your-custom-grpc-node.com", # [!code focus]

rest_indexer="https://your-custom-rest-indexer.com", # [!code focus]

websocket_indexer="wss://your-custom-websocket-indexer.com" # [!code focus]

).node # [!code focus]

# Instantiate the HTTP sub-client. # [!code focus]

indexer = IndexerClient(config.rest_indexer) # [!code focus]

# Instatiate the WebSockets sub-client, connecting to the network. # [!code focus]

socket = await IndexerSocket(network.websocket_indexer).connect() # [!code focus]

```

```typescript [TypeScript]

import { IndexerClient, Network, SocketClient } from '@dydxprotocol/v4-client-js';

const apiTimeout = 1000;

// Using a pre-configured endpoint. // [!code focus]

const config = Network.mainnet().indexerConfig; // [!code focus]

// You can modify the HTTP endpoint doing `config.restEndpoint = "...";` [!code focus]

// You can modify the WebSockets endpoint doing `config.websocketEndpoint = "...";` [!code focus]

// Instantiate the HTTP client. // [!code focus]

const indexer = new IndexerClient(config, apiTimeout); // [!code focus]

// Instantiate the WebSockets client, connecting to the network. // [!code focus]

const socket = new SocketClient( // [!code focus]

config.indexerConfig, // [!code focus]

() => {}, // onOpenCallback

() => {}, // onCloseCallback

() => {}, // onMessageCallback

() => {} // onErrorCallback

); // [!code focus]

socket.connect(); // [!code focus]

```

```rust [Rust]

use dydx::{config::ClientConfig, indexer::IndexerClient};

// The configuration file should have the endpoint. // [!code focus]

let config = ClientConfig::from_file("config.toml").await?; // [!code focus]

// Instantiate the client. // [!code focus]

// Both HTTP and WebSockets methods are provided with the `indexer`. // [!code focus]

let indexer = IndexerClient::new(config.indexer); // [!code focus]

```

:::

#### Composite client (TypeScript only)

The Composite client groups commonly used methods into a single structure. It is essentially composed by both the Node and Indexer clients.

```typescript [TypeScript]

import { CompositeClient, Network } from '@dydxprotocol/v4-client-js';

const network = Network.mainnet();

const client = await CompositeClient.connect(network); // [!code focus]

```

:::info

The Python and Rust APIs do not have a Composite client. The explicit Node and Indexer clients should be used instead.

:::

#### Faucet client

To test your trading strategy, test funds can be requested from the Faucet client. This client only works in the **testnet**. The acquired test funds can only be used in the **testnet**.

:::code-group

```python [Python]

from dydx_v4_client.network import TESTNET_FAUCET

from dydx_v4_client.faucet_client import FaucetClient

faucet = FaucetClient(TESTNET_FAUCET) # [!code focus]

```

```typescript [TypeScript]

import { FaucetApiHost, FaucetClient } from '@dydxprotocol/v4-client-js';

const client = new FaucetClient(FaucetApiHost.TESTNET); // [!code focus]

```

```rust [Rust]

// The feature `faucet` must be enabled.

use anyhow::anyhow as err;

use dydx::{config::ClientConfig, faucet::FaucetClient};

let config = ClientConfig::from_file("config.toml").await?;

let faucet = FaucetClient::new( // [!code focus]

config // [!code focus]

.faucet // [!code focus]

.ok_or_else(|| err!("The config file must contain a [faucet] config!"))?, // [!code focus]

); // [!code focus]

```

:::

#### Noble client

To move assets in and out of the dYdX network, the Noble network is commonly employed.

:::tip[Alternatives]

Moving assets is not restricted to using the Noble client directly. Please see the [Deposits and Withdrawals](/interaction/deposits-withdrawals/overview) page.

:::

:::code-group

```python [Python]

from dydx_v4_client.indexer.rest.noble_client import NobleClient

client = NobleClient("https://rpc.testnet.noble.strange.love") # [!code focus]

await client.connect(MNEMONIC) # [!code focus]

```

```typescript [TypeScript]

import { NobleClient } from '@dydxprotocol/v4-client-js';

const client = new NobleClient('https://rpc.testnet.noble.strange.love', 'Noble example'); // [!code focus]

```

```rust [Rust]

// The feature `noble` must be enabled.

use anyhow::anyhow as err;

use dydx::{config::ClientConfig, noble::NobleClient};

let config = ClientConfig::from_file("config.toml").await?;

let noble = NobleClient::connect( // [!code focus]

config // [!code focus]

.noble // [!code focus]

.ok_or_else(|| err!("The config file must contain a [noble] config!"))?, // [!code focus]

).await?; // [!code focus]

```

:::

### Endpoints

Some known endpoints are provided below. Use these to connect to the dYdX networks.

Feel free to compare the most suitable gRPC endpoint from this [status endpoint](https://grpc-status.dydx.trade/)

#### Node

Connections to the trading client to the full nodes are established using the (g)RPC protocol.

##### mainnet

##### gRPC

| Team | URI | Rate limit |

| --------- | ---------------------------------------------------------------------------------------------------------------------------------------------- | ---------- |

| OEGS | `grpc://oegs.dydx.trade:443` | |

| Polkachu | `https://dydx-dao-grpc-1.polkachu.com:443` `https://dydx-dao-grpc-2.polkachu.com:443` `https://dydx-dao-grpc-3.polkachu.com:443` | 300 req/m |

| KingNodes | `https://dydx-ops-grpc.kingnodes.com:443` | 250 req/m |

| Enigma | `https://dydx-dao-grpc.enigma-validator.com:443` | |

##### Archive gRPC

| Team | URI | Rate limit |

| --------- | --------------------------------------------------------- | ---------- |

| Polkachu | `https://dydx-dao-archive-grpc-1.polkachu.com:443` | 300 req/m |

| KingNodes | `https://dydx-ops-archive-grpc.kingnodes.com:443` | 250 req/m |

| Enigma | `https://dydx-dao-grpc-archive.enigma-validator.com:1492` | |

##### RPC

| Team | URI | Rate limit |

| --------- | ----------------------------------------------- | ---------- |

| OEGS | `https://oegs.dydx.trade:443` | |

| Polkachu | `https://dydx-dao-rpc.polkachu.com:443` | 300 req/m |

| KingNodes | `https://dydx-ops-rpc.kingnodes.com:443` | 250 req/m |

| Enigma | `https://dydx-dao-rpc.enigma-validator.com:443` | |

##### Archive RPC

| Team | URI | Rate limit |

| --------- | -------------------------------------------------------- | ---------- |

| Polkachu | `https://dydx-dao-archive-rpc.polkachu.com:443` | 300 req/m |

| KingNodes | `https://dydx-ops-archive-rpc.kingnodes.com:443 ` | 250 req/m |

| Enigma | `https://dydx-dao-rpc-archive.enigma-validator.com:443 ` | |

##### REST

| Team | URI | Rate limit |

| --------- | ----------------------------------------------- | ---------- |

| Polkachu | `https://dydx-dao-api.polkachu.com:443` | 300 req/m |

| KingNodes | `https://dydx-ops-rest.kingnodes.com:443` | 250 req/m |

| Enigma | `https://dydx-dao-lcd.enigma-validator.com:443` | |

##### Archive REST

| Team | URI | Rate limit |

| --------- | ------------------------------------------------------- | ---------- |

| Polkachu | `https://dydx-dao-archive-api.polkachu.com:443` | 300 req/m |

| KingNodes | `https://dydx-ops-archive-rest.kingnodes.com:443` | 250 req/m |

| Enigma | `https://dydx-dao-lcd-archive.enigma-validator.com:443` | |

##### testnet

##### gRPC

| Team | URI |

| --------- | -------------------------------------------------- |

| OEGS | `oegs-testnet.dydx.exchange:443` |

| KingNodes | `test-dydx-grpc.kingnodes.com:443 (TLS)` |

| Polkachu | `dydx-testnet-grpc.polkachu.com:23890 (plaintext)` |

##### RPC

| Team | URI |

| --------- | ----------------------------------------------- |

| OEGS | `https://oegs-testnet.dydx.exchange:443` |

| Enigma | `https://dydx-rpc-testnet.enigma-validator.com` |

| KingNodes | `https://test-dydx-rpc.kingnodes.com` |

| Polkachu | `https://dydx-testnet-rpc.polkachu.com` |

##### REST

| Team | URI |

| --------- | ----------------------------------------------- |

| Enigma | `https://dydx-lcd-testnet.enigma-validator.com` |

| KingNodes | `https://test-dydx-rest.kingnodes.com` |

| Polkachu | `https://dydx-testnet-api.polkachu.com` |

#### Indexer

Connections with the Indexer are established either using HTTP (for spontaneuous data retrieval) or WebSockets (for data streaming).

##### mainnet

| Type | URI |

| ---- | -------------------------------- |

| HTTP | `https://indexer.dydx.trade/v4` |

| WS | `wss://indexer.dydx.trade/v4/ws` |

##### testnet

| Type | URI |

| ---- | --------------------------------------------- |

| HTTP | `https://indexer.v4testnet.dydx.exchange` |

| WS | `wss://indexer.v4testnet.dydx.exchange/v4/ws` |

#### Faucet

Used to retrieve test funds.

##### testnet

`https://faucet.v4testnet.dydx.exchange`

#### Noble

Connections with the Noble blockchain. Similarly to the dYdX networks, Noble also has a **mainnet** and a **testnet**.

##### mainnet

| Team | URI |

| -------- | -------------------------------------------------- |

| Polkachu | `http://noble-grpc.polkachu.com:21590 (plaintext)` |

##### testnet

| Team | URI |

| -------- | --------------------------------------------------- |

| Polkachu | `noble-testnet-grpc.polkachu.com:21590 (plaintext)` |

:::info

In the Cosmos blockchains (dYdX, Noble, etc.) inter-blockchain communications require IBC relayers to be present that facilitate bridging between networks.

These IBC relayers may not be active, specially for the **testnet** networks.

:::

## Guide

import Details from '../../components/Details';

## Wallet Setup

To manage your accounts, issue orders, and perform other operations that are required to be signed, a Wallet is required. To instantiate a Wallet, you must first have your associated **mnemonic**.

* The Python client requires the use of an address to setup the Wallet. However, the address can only be fetched using a Wallet. The address is derived from the mnemonic (address \< public key \< private key \< mnemonic).

* Wallet, accounts, subaccounts are all handled differently among the clients. Probably the Rust client handles this best, giving the user more control:

1. There is a `Wallet`;

2. The `Wallet` is used to derive an `Account` by index (each `Account` is associated with a keypair);

3. An `Account` is used to derive a `Subaccount` by index. A `Subaccount` is employed to create orders.

::::steps

### Getting the mnemonic

A Wallet is setup using your secret **mnemonic** phrase. A **mnemonic** is a set of 24 words to back up and access your account.

You can fetch your **mnemonic** from the [dYdX Frontend](https://dydx.trade). After logging in, follow the instructions in "Export secret phrase", accessed by clicking your address in the upper right corner.

For the purpose of this guide, lets copy and store the **mnemonic** in a `mnemonic.txt` file.

:::warning

Handle your **mnemonic** in a secure manner. **Do not share** it with other parties. Do not commit your **mnemonic** to a public VCS like GitHub. Access to your **mnemonic** provides access to your account and funds.

:::

### Read the mnemonic

Lets start coding. Load the mnemonic into a string variable. This assumes the mnemonic is stored in a text file.

:::code-group

```python [Python]

mnemonic = open('mnemonic.txt').read().strip()

```

```typescript [TypeScript]

const mnemonic = require('fs').readFileSync('mnemonic.txt', 'utf8').trim();

```

```rust [Rust]

let mnemonic = std::fs::read_to_string("mnemonic.txt").unwrap().trim().to_string();

```

:::

### Create the Wallet

Use the **mnemonic** to create a Wallet instance capable of signing transactions.

:::code-group

```python [Python]

from dydx_v4_client.key_pair import KeyPair

from dydx_v4_client.wallet import Wallet

# Define your address.

address = Wallet(KeyPair.from_mnemonic(mnemonic), 0, 0).address()

# Create a Wallet with updated parameters required for trading

wallet = await Wallet.from_mnemonic(node, mnemonic, address)

```

```typescript [TypeScript]

import { BECH32_PREFIX, LocalWallet } from '@dydxprotocol/v4-client-js';

const wallet = await LocalWallet.fromMnemonic(mnemonic, BECH32_PREFIX);

```

```rust [Rust]

use dydx::node::Wallet;

let wallet = Wallet::from_mnemonic(&mnemonic)?;

```

:::

:::note

Please check the list of [available endpoints here](/interaction/endpoints#endpoints).

:::

### Instantiate a Subaccount

:::note

This step is not required in the Python client.

:::

When issuing orders, the relevant Subaccount must be chosen to place the order under. A Subaccount is associated with an Account, and is meant to provide trade isolation against your other Subaccounts and enhance funds management.

See more about [Accounts and Subaccounts](/concepts/trading/accounts).

:::code-group

```python [Python]

# Not required. The `wallet` instance created above already contains the necessary information.

# The Subaccount to be used is defined using an integer when creating an order.

```

```typescript [TypeScript]

import { SubaccountInfo } from '@dydxprotocol/v4-client-js';

const subaccount = new SubaccountInfo(wallet, 0);

```

```rust [Rust]

// Create an `Account` instance for the account index 0. This `Account` has updated parameters required for trading.

let account = wallet.account(0, &mut node).await?;

// Create a `Subaccount` instance for the subaccount index 0.

let subaccount = account.subaccount(0)?;

```

:::

:::info

By default, both Python and TypeScript client Wallets will derive and use the Account indexed at 0.

:::

::::

#### Connect

Connect the Noble client to the Noble network.

##### Method Declaration

:::code-group

```python [Python]

async def connect(self, mnemonic: str)

```

```rust [Rust]

pub async fn connect(config: NobleConfig) -> Result

```

```typescript [Typescript]

async connect(wallet: LocalWallet): Promise

```

```url [API]

```

:::

##### Parameters

##### Response

Examples: [TypeScript] | [Rust]

[Rust]: https://github.com/dydxprotocol/v4-clients/blob/3e8c7e1b960291b7ef273962d374d9934a5c4d33/v4-client-rs/client/examples/wallet.rs#L89

[TypeScript]: https://github.com/dydxprotocol/v4-clients/blob/3e8c7e1b960291b7ef273962d374d9934a5c4d33/v4-client-js/examples/noble_example.ts#L19

#### Get account

Query for [an account](https://github.com/cosmos/cosmos-sdk/tree/main/x/auth#account-1) by it's address.

##### Method Declaration

:::code-group

```python [Python]

async def get_account(self, address: str) -> BaseAccount

```

```rust [Rust]

pub async fn get_account(&mut self, address: &Address) -> Result

```

```typescript [TypeScript]

```

```url [API]

```

:::

##### Parameters

##### Response

Examples: [Python] | [Rust]

[Python]: https://github.com/dydxprotocol/v4-clients/blob/3e8c7e1b960291b7ef273962d374d9934a5c4d33/v4-client-py-v2/examples/basic_adder.py#L159

[Rust]: https://github.com/dydxprotocol/v4-clients/blob/3e8c7e1b960291b7ef273962d374d9934a5c4d33/v4-client-rs/client/examples/wallet.rs#L89

#### Get Account Balance

Query token balance of an account/address.

##### Method Declaration

:::code-group

```python [Python]

async def get_account_balance(

self, address: str, denom: str

) -> bank_query.QueryBalanceResponse

```

```rust [Rust]

pub async fn get_account_balance(

&mut self,

address: Address,

denom: &Denom,

) -> Result

```

```typescript

getAccountBalance(denom: string): Promise

```

```url [API]

```

:::

##### Parameters

##### Response

Examples: [TypeScript]

[TypeScript]: https://github.com/dydxprotocol/v4-clients/blob/3e8c7e1b960291b7ef273962d374d9934a5c4d33/v4-client-js/examples/noble_example.ts#L93

#### Get Account Balances

Query all balances of an account/address.

##### Method Declaration

:::code-group

```python [Python]

async def get_account_balances(

self, address: str

) -> bank_query.QueryAllBalancesResponse:

```

```rust [Rust]

pub async fn get_account_balances(&mut self, address: Address) -> Result, Error>

```

```typescript [TypeScript]

getAccountBalances(): Promise

```

:::

##### Parameters

##### Response

Examples: [TypeScript] | [Rust]

[Rust]: https://github.com/dydxprotocol/v4-clients/blob/3e8c7e1b960291b7ef273962d374d9934a5c4d33/v4-client-rs/client/examples/noble_transfer.rs#L62

[TypeScript]: https://github.com/dydxprotocol/v4-clients/blob/3e8c7e1b960291b7ef273962d374d9934a5c4d33/v4-client-js/examples/noble_example.ts#L58

import NobleClient from './intro.mdx'

import Connect from './connect.mdx'

import GetAccountBalance from './get_account_balance.mdx'

import GetAccountBalances from './get_account_balances.mdx'

import GetAccount from './get_account.mdx'

import QueryAddress from './query_address.mdx'

import SendTokenIbc from './send_token_ibc.mdx'

import Simulate from './simulate.mdx'

## Noble API

### Methods

#### Query Address

Fetch account's number and sequence number from the network.

##### Method Declaration

:::code-group

```python [Python]

async def query_address(self, address: str) -> (int, int)

```

```rust [Rust]

pub async fn query_address(&mut self, address: &Address) -> Result<(u64, u64), Error>

```

```typescript [TypeScript]

```

:::

##### Parameters

##### Response

import Details from '../../components/Details';

#### Send Token Ibc

Transfer a token asset between Cosmos blockchain networks.

##### Method Declaration

:::code-group

```python [Python]

```

```rust [Rust]

pub async fn send_token_ibc(

&mut self,

account: &mut Account,

sender: Address,

recipient: Address,

token: impl Tokenized,

source_channel: String,

) -> Result

```

```typescript [TypeScript]

async IBCTransfer(message: MsgTransferEncodeObject): Promise

async send(

messages: EncodeObject[],

gasPrice: GasPrice = GasPrice.fromString('0.1uusdc'),

memo?: string,

): Promise

```

```url [API]

/ibc.applications.transfer.v1.Msg/Transfer

```

:::

* Generalize to all IBC/blockchains.

* Missing in Python.

* Missing in TS: user required to produce the low-level message and then `post.send()` it.

##### Parameters

| Parameter | Location | Type | Mandatory | Description |

| ---------------- | -------- | --------- | --------- | ---------------------------------- |

| `account` | query | [Account] | true | The account. |

| `sender` | query | [Address] | true | Address of the sender. |

| `recipient` | query | [Address] | true | Address of the recipient. |

| `token` | query | int | true | Token type and amount to transfer. |

| `source_channel` | query | String | true | Source IBC relay channel. |

##### Response

| Status | Meaning | Schema | |

| ------ | ------------- | -------- | ------------------------------------- |

| `200` | [OK] | [TxHash] | |

| `400` | [Bad Request] | | The request was malformed or invalid. |

[OK]: /types/ok

[Account]: /types/account

[Address]: /types/address

[TxHash]: /types/tx_hash

[Bad Request]: /types/bad-request

#### Simulate

##### Method Declaration

:::code-group

```python [Python]

async def simulate_transaction(

self,

messages: List[dict],

gas_price: str = "0.025uusdc",

memo: Optional[str] = None,

) -> Fee:

```

```rust [Rust]

async fn simulate(&mut self, tx_raw: &tx::Raw) -> Result

```

```typescript [TypeScript]

async simulateTransaction(

messages: readonly EncodeObject[],

gasPrice: GasPrice = GasPrice.fromString('0.1uusdc'),

memo?: string,

): Promise

```

:::

##### Parameters

##### Response

Examples: [TypeScript]

[TypeScript]: https://github.com/dydxprotocol/v4-clients/blob/3e8c7e1b960291b7ef273962d374d9934a5c4d33/v4-client-js/examples/noble_example.ts#L78

## Node API

Nodes are the servers that manage and maintain the dYdX network. Trading transactions are broadcast to these, which then are evaluated and eventually comitted into state by the underlying consensus mechanim. It serves both a [Private API](/node-client/private), which receives transactions signed by the user, and a [Public API](/node-client/public), available for different data queries. The [Permissioned Keys API](/node-client/authenticators) is also available.

See the [guide](/interaction/endpoints#node-client) on how to use the available Node client to learn how to connect to it.

:::tip

Consider using the [Indexer API](/indexer-client) over the Node Public API for data queries.

:::

## Network Constants

### Chain ID

**mainnet**: `dydx-mainnet-1`

**testnet**: `dydx-testnet-4`

### Native Token Denom

**mainnet**: `adydx`

**testnet**: `adv4tnt`

### Chain Registry

**mainnet**: `dydx`

**testnet**: `dydxtestnet`

## Resources

### `networks` Repositories

mainnet: [https://github.com/dydxopsdao/networks/tree/main/dydx-mainnet-1](https://github.com/dydxopsdao/networks/tree/main/dydx-mainnet-1)

testnet: [https://github.com/dydxprotocol/v4-testnets/tree/main/dydx-testnet-4](https://github.com/dydxprotocol/v4-testnets/tree/main/dydx-testnet-4)

### Upgrades History

:::details[mainnet]

| Block Height | Proposal | Compatible Versions | Comments |

| ------------------------ | -------- | --------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------- | ----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------- |

| 1 \~ 1,805,000 | N/A | [v2.0.1](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv2.0.1) [v1.0.1](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv1.0.1) [v1.0.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv1.0.0) | `v1.0.1` was a rolling upgrade; `v2.0.1` was backported to enable easier syncing from block 1 |

| 1,805,001 \~ 7,147,831 | N/A | [v2.0.1](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv2.0.1) [v2.0.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv2.0.0) | `v2.0.0` was an emergency fix |

| 7,147,832 \~ 12,791,711 | 7 | [v3.0.2](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv3.0.2) [v3.0.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv3.0.0) | `v3.0.2` allows easier syncing from block 1 |

| 12,791,712 \~ 14,404,199 | 46 | [v4.0.5](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv4.0.5) | |

| 14,404,200 \~ 17,559,999 | 53 | [v4.1.2](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv4.1.2) [v4.1.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv4.1.0) | `v4.1.2` adds performance improvements |

| 17,560,000 \~ 21,141,999 | 59 | [v5.0.6](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv5.0.6) [v5.0.4](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv5.0.4) [v5.0.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv5.0.0) | `v5.0.4` adds performance improvements `v5.0.6` fixes a chain liveness issue |

| 21,142,000 \~ 22,169,999 | 125 | [v5.1.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv5.1.0) | |

| 22,170,000 \~ 26,784,999 | 130 | [v5.2.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv5.2.0) | |

| 26,785,000 \~ 29,949,999 | 160 | [v6.0.4](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv6.0.4) [v6.0.9](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv6.0.9) | `v6.0.9` a Comet Security patch `v6.0.4` Integrates and adds Marketmap functionality, expands transaction sequence number validation to accept timestamp nonces, and introduces individual vault parameters. |

| 29,950,000 \~ 35,601,999 | 173 | [v7.0.1](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv7.0.1) | `v7.0.1`

|

| 56,530,000 \~ 58,492,678 | 283 | [v9.1.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv9.1.0) | `v9.1.0` Fixes validator set hash computation to match standard CometBFT |

| 58,492,679 \~ 59,834,999 | N/A | [v9.2.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv9.2.0) [9.2.1](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv9.2.1) | `v9.2.0` The chain expereinced a halt at height 58,492,678 and needed emergency patching `v9.2.1` applies a Cosmos-SDK security patch |

| 59,835,000 \~ 62,249,999 | 303 | [v9.3.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv9.3.0) | `v9.3.0` Permanent fix for the chain halt at height 58,492,678 |

| 62,250,000 \~ 66,629,999 | 303 | [v9.4.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv9.4.0) | `v9.4.0` Leverage enforcement, staking-based fee tiers, and refined affiliate rewards |

| 66,630,000 \~ 73,859,999 | 323 | [v9.5.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv9.5.0) | `v9.5.0` Governance-controlled transfer mechanism, epoch querying commands, and short block window parameter adjustments |

| 73,860,000 \~ | 342 | [v9.6.1](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv9.6.1) [v9.6.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv9.6.0) | `v9.6.0` Governance controls for perpetual market step and tick sizes `v9.6.1` Dependency bumps for security fixes |

:::

:::details[testnet]

| Block Height | Proposal | Compatible Versions | Comments |

| ------------------------ | -------- | ------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------ | ---------------------------------------- |

| 1 \~ 4,999,999 | N/A | [v2.0.1](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv2.0.1) [v2.0.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv2.0.0) [v1.0.1](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv1.0.1) [v1.0.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv1.0.0) | The chain was never upgraded to `v2.0.0` |

| 5,000,000 \~ 6,879,999 | 18 | [v3.0.2](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv3.0.2) [v3.0.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv3.0.0) | |

| 6,880,000 \~ 10,449,999 | 45 | [v4.0.5](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv4.0.5) | |

| 10,450,000 \~ 12,071,999 | 73 | [v4.1.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv4.1.0) | |

| 12,072,000 \~ 16,291,699 | 82 | [v5.0.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv5.0.0) | |

| 16,291,700 \~ 17,706,999 | 110 | [v5.1.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv5.1.0) | |

| 17,707,000 \~ 19,487,299 | 113 | [v5.2.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv5.2.0) | |

| 19,487,300 \~ 20,579,999 | 185 | [v6.0.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv6.0.0) | |

| 20,580,000 \~ 21,669,999 | 208 | [v6.0.3-rc0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv6.0.3-rc0) | |

| 21,670,000 \~ 23,527,799 | 222 | [v6.0.4-rc2](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv6.0.4-rc2) | |

| 23,527,800 \~ 28,234,999 | 227 | [v7.0.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv7.0.0) | |

| 28,235,000 \~ 42,857,847 | 266 | [v8.0.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv8.0.0) | |

| 42,857,848 \~ 43,913,064 | 307 | [v8.1.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv8.1.0) | |

| 43,913,065 \~ 46,589,845 | 310 | [v8.2.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv8.2.0) | |

| 46,589,846 \~ 49,045,932 | 313 | [v9.0.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv9.0.0) | |

| 49,045,933 \~ 51,610,520 | 337 | [v9.1.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv9.1.0) | |

| 51,610,521 \~ 52,967,285 | 342 | [v9.3.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv9.3.0) | |

| 52,967,286 \~ 56,861,499 | 345 | [v9.4.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv9.4.0) | |

| 56,861,500 \~ 60,703,999 | 360 | [v9.5.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv9.5.0) | |

| 60,704,000 \~ | 368 | [v9.6.0](https://github.com/dydxprotocol/v4-chain/releases/tag/protocol%2Fv9.6.0) | |

:::

### Seed Nodes

:::details[mainnet]

| Team | URI |

| ---------- | ------------------------------------------------------------------------------- |

| Polkachu | `ade4d8bc8cbe014af6ebdf3cb7b1e9ad36f412c0@seeds.polkachu.com:23856` |

| KingNodes | `df1f145848d253800d4e4216e8793158688912f1@seeds.kingnodes.com:23856` |

| Enigma | `6a720a1e5e8be9acf2752b22dc868ea2f95aaaf7@dydx-seeds.enigma-validator.com:1490` |

| CryptoCrew | `c2c2fcb5e6e4755e06b83b499aff93e97282f8e8@tenderseed.ccvalidators.com:26401` |

:::

:::details[testnet]

| Team | URI |

| ----------- | --------------------------------------------------------------------------------------- |

| AllThatNode | `19d38bb5cea1378db3e16615e63594dc26119a1a@dydx-testnet4-seednode.allthatnode.com:26656` |

| Crosnest: | `87ee8de5f0f82af6ee6740a30f8844bbe6434413@seed.dydx-testnet.cros-nest.com:26656` |

| CryptoCrew: | `38e5a5ec34c578dc323cbdd9b98330abb448d586@tenderseed.ccvalidators.com:29104` |

:::

### Indexer Endpoints

See [Endpoints](/interaction/endpoints#indexer).

### State Sync Nodes

:::details[mainnet]

| Team | State Sync Peers | Region |

| --------- | ----------------------------------------------------------------------- | ------- |

| Polkachu | `580ec248de1f41d4e50abe132b7838348db55b80@176.9.144.40:23856` | Germany |

| Polkachu | `90b0ee8e73d8237b06356b244ff9854d1991a1f8@65.109.115.228:23856` | Finland |

| Polkachu | `874b5ab53d8f5edae6674ad394f20e2b297cf73f@199.254.199.182:23856` | Japan |

| KingNodes | `92266f1badca0ca332d2f0a178f040050b873267@5.61.208.101:238566` | APAC |

| KingNodes | `4ebd98a10a76ccbec97714ac4435cb6315fc4dbb@57.129.53.67:23856` | EU |

| Enigma | `6a720a1e5e8be9acf2752b22dc868ea2f95aaaf7@135.181.183.118:1490` | Finland |

| Enigma | `4e7ad7c7a8e8054d2005ea669b9329934882b58c@136.243.35.160:1490` | Germany |

| Enigma | `477d6e72440e02fc99aaa9b67a0d2903a53da350@15.235.227.122:1490` | Japan |

:::

:::details[testnet]

| Team | State Sync Peers |

| -------- | -------------------------------------------------------------- |

| Polkachu | `0d17772cbba3b488ad895b17b9a48948e480b1fa@65.109.23.114:23856` |

:::

### Snapshot Service

:::details[mainnet]

| Team | URI | Pruning | Index |

| --------- | ------------------------------------------------------------------ | ------- | ----- |

| Polkachu | `https://polkachu.com/tendermint_snapshots/dydx` | Yes | null |

| KingNodes | `https://snapshots.kingnodes.com/network/dydx` | No | kv |

| Enigma | `https://enigma-validator.com/networks?asset=dydx#networkservices` | Yes | |

:::

:::details[testnet]

| Team | URI | Pruning | Index |

| -------- | -------------------------------------------------- | ------- | ----- |

| Polkachu | `https://www.polkachu.com/testnets/dydx/snapshots` | Yes | null |

:::

### Live Peer Node Providers

:::details[mainnet]

| Team | URI |

| -------- | -------------------------------------- |

| Polkachu | `https://polkachu.com/live_peers/dydx` |

:::

### Address Book Providers

:::details[mainnet]

| Team | URI |

| -------- | ------------------------------------- |

| Polkachu | `https://polkachu.com/addrbooks/dydx` |

:::

### Full Node Endpoints

See [Endpoints](/interaction/endpoints#node).

### Archival Node Endpoints

:::details[mainnet]

**RPC**

| Team | URI | Rate limit |

| --------- | ------------------------------------------------------- | ---------- |

| Polkachu | `https://dydx-dao-archive-rpc.polkachu.com:443` | 300 req/m |

| KingNodes | `https://dydx-ops-archive-rpc.kingnodes.com:443` | 50 req/m |

| Enigma | `https://dydx-dao-rpc-archive.enigma-validator.com:443` | |

**REST**

| Team | URI | Rate limit |

| --------- | ------------------------------------------------------- | ---------- |

| Polkachu | `https://dydx-dao-archive-api.polkachu.com:443` | 300 req/m |

| KingNodes | `https://dydx-ops-archive-rest.kingnodes.com:443` | 50 req/m |

| Enigma | `https://dydx-dao-lcd-archive.enigma-validator.com:443` | |

**gRPC**

| Team | URI | Rate limit |

| --------- | ------------------------------------------------------------------------------------------------------------ | ---------- |

| Polkachu | `https://dydx-dao-archive-grpc-1.polkachu.com:443` `https://dydx-dao-archive-grpc-2.polkachu.com:443` | 300 req/m |

| KingNodes | `https://dydx-ops-archive-grpc.kingnodes.com:443` | 50 req/m |

| Enigma | `https://dydx-dao-grpc-archive.enigma-validator.com:1492` | |

:::

:::details[testnet]

No Archival Nodes.

:::

### Other Links

:::details[mainnet]

| Name | URI |

| --------------------------- | ------------------------------------------------------------------------------------------------------ |

| dYdX Chain Web Frontend | `https://dydx.trade/` |

| Status Page | `https://status.dydx.trade` |

| Mintscan | `https://www.mintscan.io/dydx` |

| Keplr | `https://wallet.keplr.app/chains/dydx` |

| Validator Metrics | `https://p.ap1.datadoghq.com/sb/610e1836-51dd-11ee-a995-da7ad0900009-78607847ff8632d8a96737ed3437f40c` |

| #validators Discord Channel | `https://discord.com/channels/724804754382782534/1029585380170805379` |

| FE Bug Report Form | `https://www.dydxopsdao.com/feedback` |

:::

:::details[testnet]

| Name | URI |

| -------------------------- | ----------------------------------------------------------------------------------------------------- |

| Public Testnet Front End | `https://v4.testnet.dydx.exchange` |

| Status Page | `https://status.v4testnet.dydx.exchange` |

| Mintscan | `https://www.mintscan.io/dydx-testnet` |

| Keplr | `https://testnet.keplr.app/chains/dydx-testnet` |

| Validator Metrics | `https://p.datadoghq.com/sb/dc160ddf0-05a98d2dbe2a01d8caa5783eb616f826` |

| Discord Channel (Feedback) | `https://discord.com/channels/724804754382782534/1117897181886677012` |

| Google Form (Feedback) | `https://docs.google.com/forms/d/e/1FAIpQLSezLsWCKvAYDEb7L-2O4wOON1T56xxro9A2Azvl6IxXHP_15Q/viewform` |

:::

## Security

### Independent Audits

The protocol has been audited by the [Informal Systems](https://informal.systems/) team. Additional audits are planned as more protocol code is developed.

You can find all finalized audit reports in the [v4\_chain audits folder](https://github.com/dydxprotocol/v4-chain/tree/main/audits).

### Bug Bounty

With all core dYdX Chain (v4) software GitHub repos now made public, we are inviting the community to help us identify any vulnerabilities to improve the security of dYdX Chain.

To find more details, please see our blog post [here](https://dydx.exchange/blog/dydx-bug-bounty-program)!

## Terms-of-Use & Privacy Policy

By using, recording, referencing, or downloading (i.e., any “action”) any information contained on this page or in any dYdX Trading Inc. ("dYdX") database or documentation, you hereby and thereby agree to the [v4 Terms of Use](https://dydx.exchange/v4-terms) and [Privacy Policy](https://dydx.exchange/privacy) governing such information, and you agree that such action establishes a binding agreement between you and dYdX.

This documentation provides information on how to use dYdX v4 software (”dYdX Chain”). dYdX does not deploy or run v4 software for public use, or operate or control any dYdX Chain infrastructure. dYdX is not responsible for any actions taken by other third parties who use v4 software. dYdX services and products are not available to persons or entities who reside in, are located in, are incorporated in, or have registered offices in the United States or Canada, or Restricted Persons (as defined in the dYdX [Terms of Use](https://dydx.exchange/terms)). The content provided herein does not constitute, and should not be construed, or relied upon as, financial advice, legal advice, tax advice, investment advice or advice of any other nature, and you agree that you are responsible to conduct independent research, perform due diligence and engage a professional advisor prior to taking any financial, tax, legal or investment action related to the foregoing content. The information contained herein, and any use of v4 software, are subject to the [v4 Terms of Use](https://dydx.exchange/v4-terms).

#### Method Name

// TODO: Add description

##### Method Declaration

:::code-group

```rust [Rust]

```

```python [Python]

```

```typescript [TypeScript]

```

```url [API]

```

:::

##### Parameters

| Parameter | Location | Type | Required | Description |

| --------- | -------- | ---- | -------- | ----------- |

| | | | | |

##### Response

| Status | Meaning | Description | Schema |

| ------ | ------- | ----------- | ------ |

| | | | |

## Indexer Deep Dive

A good way to think about the Indexer is as similar to Infura or Alchemy’s role in the Ethereum ecosystem. However, unlike Infura/Alchemy, and like everything else in dYdX Chain, the Indexer is completely open source and can be run by anyone!

#### What is the Indexer?

As part of tooling for the dYdX ecosystem, we want to ensure that clients have access to performant data queries when using exchanges running on dYdX Chain software. Cosmos SDK Full Nodes offer a number of APIs that can be used to request onchain data. However, these Full Nodes are optimized for committing and executing blocks, not for serving high frequency, low-latency requests from web/mobile clients.

This is why we wrote software for an indexing service. The Indexer is a read-only service that serves off chain data to clients over REST APIs and Websockets. Its purpose is to store and serve data that exists on dYdX Chain in an easier to use way. In other words, the purpose of an indexer is to index and serve data to clients in a more performant, efficient and web2-friendly way. For example the indexer will serve websockets that provide updates on the state of the orderbook and fills. These clients will include front-end applications (mobile and web), market makers, institutions, and any other parties looking to query dYdX Chain data via a traditional web2 API.

#### Onchain vs. Offchain data

The Indexer will run two separate ingestion/storage processes with data from a v4 Full Node: one for onchain data and one for offchain data. Currently, throughput of onchain data state changes is expected to be from 10-50 events/second. On the other hand, the expected throughput of offchain data state changes is between 500-1,000 events/second. This represents a 10-100x difference in throughput requirements. By handling these data types separately, v4 is built to allow for different services to better scale according to throughput requirements.

#### Onchain Data

Onchain data is all data that can be reproduced by reading committed transactions on a dYdX Chain deployment. All onchain data has been validated through consensus. This data includes:

1. Account balances (USDC)

2. Account positions (open interest)

3. Order Fills

1. Trades

2. Liquidations

3. Deleveraging

4. Partially and completely filled orders

4. Funding rate payments

5. Trade fees

6. Historical oracle prices (spot prices used to compute funding and process liquidations)

7. Long-term order placement and cancellation

8. Conditional order placement and cancellation

#### Offchain Data

Offchain data is data that is kept in-memory on each v4 node. It is not written to the blockchain or stored in the application state. This data cannot be queried via the gRPC API on v4 nodes, nor can it be derived from data stored in blocks. It is effectively ephemeral data on the v4 node that gets lost on restarts/purging of data from in-memory data stores. This includes:

1. Short-term order placement and cancellations

2. Order book of each perpetual exchange pair

3. Indexed order updates before they hit the chain

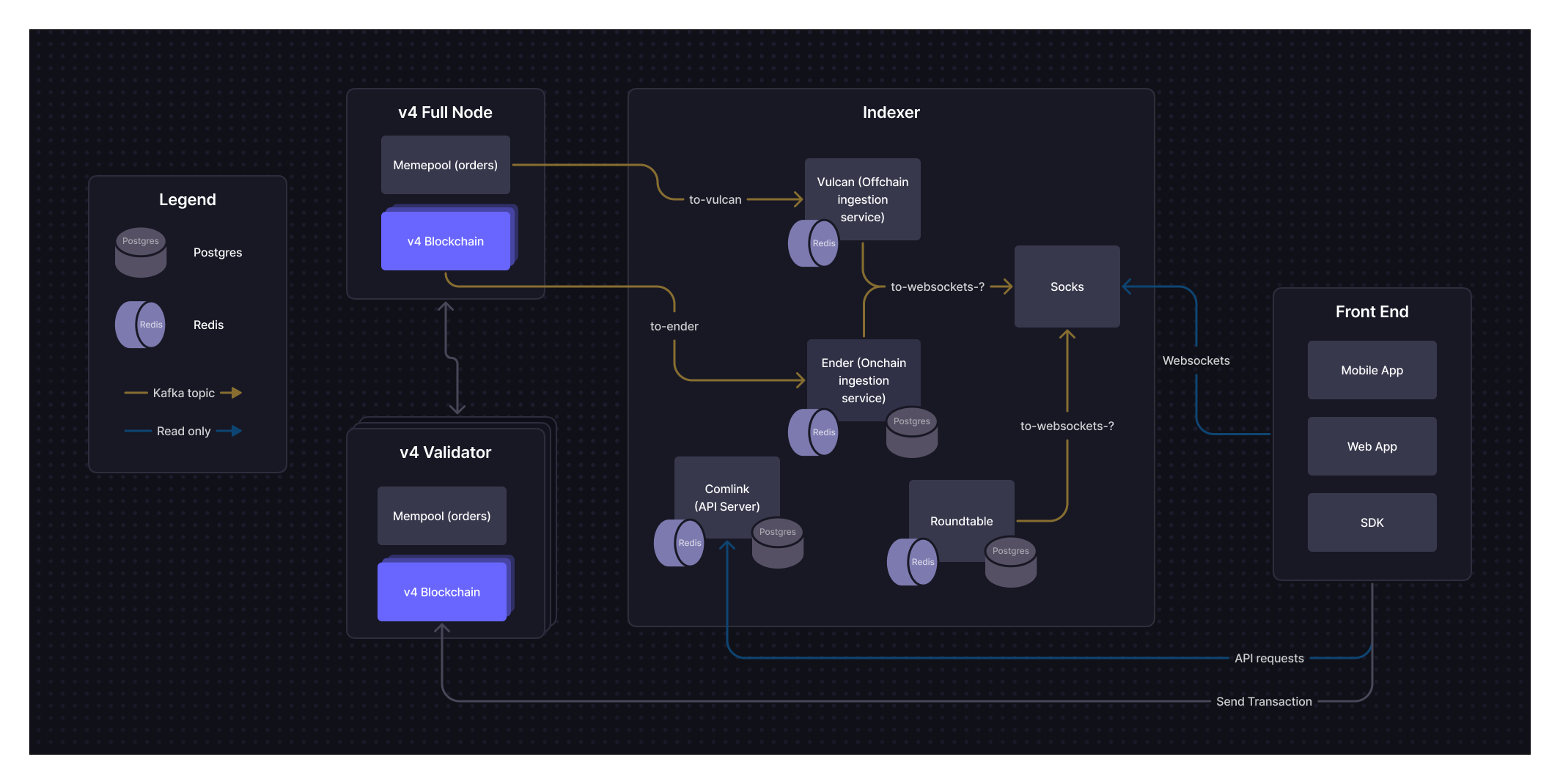

### Indexer Architecture

The Indexer is made up of a series of services that ingest information from v4 Full Nodes and serve that information to various clients. Kafka topics are used to pass events/data around to the services within the Indexer. The key services that make up Indexer are outlined below.

#### Ender (Onchain ingestion)

Ender is the Indexer’s onchain data ingestion service. It consumes data from the “to-ender” Kafka topic (which queues all onchain events by block) and each payload will include all event data for an entire block. Ender takes all state changes from that block and applies them to a Postgres database for the Indexer storing all onchain data. Ender will also create and send websocket events via a “to-websocket-?” Kafka topic for any websocket events that need to be emitted.

#### Vulcan (Offchain ingestion)

Vulcan is the Indexer’s offchain data ingestion service. It will consume data from the “to-vulcan” Kafka topic (queues all offchain events), which will carry payloads that include active order book updates, place order updates, cancel order updates, and optimistic fills. This data will be stored in a Redis cache. Vulcan will update Redis with any new open orders, set the status of canceled orders to cancel pending, and update orderbooks based on the payload received. Vulcan will also update Postgres whenever a partially filled order is canceled to update the state of the order in Postgres. Vulcan will also create and send websocket events via a “to-websocket-?” Kafka topic for any websocket events that need to be emitted.

#### Comlink (API Server)

Comlink is an API server that will expose REST API endpoints to read both onchain and offchain data. For example, a user could request their USDC balance or the size of a particular position through Comlink, and would receive a formatted JSON response.

As an explicit goal set out by the dYdX team, we’re designing v4 APIs to closely match the [v3 APIs](https://dydx.exchange/blog/v4-deep-dive-indexer#:~\:text=closely%20match%20the-,v3%20exchange%20APIs,-.%20We%20have%20had). We have had time to gather feedback and iterate on these APIs over time with v3, and have confidence that they are reasonable at the product-level.

#### Roundtable

Roundtable is a periodic job service that provides required exchange aggregation computations. Examples of these computations include: 24h volume per market, open interest, PnL by account, candles, etc.

#### Socks (Websocket service)

Socks is the Indexer’s websockets service that allows for real-time communication between clients and the Indexer. It will consume data from ender, vulcan, and roundtable, and send websocket messages to connected clients.

### Hosting & Deploying the Indexer

In service of creating an end-to-end decentralized product, the Indexer will be open source. This will include comprehensive documentation about all services and systems, as well as infrastructure-as-code for running the Indexer on popular cloud providers.

The specific responsibilities of a third party operator looking to host the Indexer generally include initial deployment and ongoing maintenance.

Initial deployment will involve:

* Setting up AWS infrastructure to utilize the open-source repo.

* Deploying Indexer code to ingest data from a full-node and expost that information through APIs and websockets

* Datadog (provides useful metrics and monitoring for Indexer services), and Bugsnag (real-time alerting on bugs or issues requiring human intervention).

Maintenance of the Indexer will involve:

* Migrating and/or upgrading the Indexer for new open-source releases

* Monitoring Bugsnag and Datadog for any issues and alerting internal team to address

* Debugging and fixing any issues with a run book provided by dYdX

dYdX believes that, at minimum, a DevOps engineer will be required to perform the necessary duties for deployment and maintenance of the Indexer. An operator will need to utilize the services below:

* AWS

* ECS - Fargate

* RDS - Postgres Database

* EC2

* Lambda

* ElastiCache Redis

* EC2 ELB - Loadbalancer

* Cloudwatch - Logs

* Secret Manager

* Terraform Cloud - for deploying to the cloud

* Bugsnag - bug awareness

* Datadog - metrics and monitoring

* Pagerduty - alerting

Operators should be able to host the open-sourced Indexer for public access in a highly available (i.e., high uptime) manner. Requirements include owning accounts to the services above and hiring the appropriate personnel to perform deployment and maintenance responsibilities.

## OEGS

### What is the Order Entry Gateway Service (OEGS)

The Order Entry Gateway represents the next step in dYdX’s multi-stage performance evolution:

1. Designated proposers — A governance-selected subset of validators responsible for proposing blocks. This creates a predictable topology for faster routing (available in v9 software upgrade).

2. Order Entry Gateway Service (OEGS) — specialized nodes for direct, one-hop delivery to proposers (available after v9 upgrade).

The Order Entry Gateway Service (OEGS) is open-sourced infrastructure that provides a direct, optimized path from traders to the proposer set, reducing latency, increasing throughput, and lowering barriers for professional and retail traders alike.

OEGS is now live on testnet, reach out to us for more information.

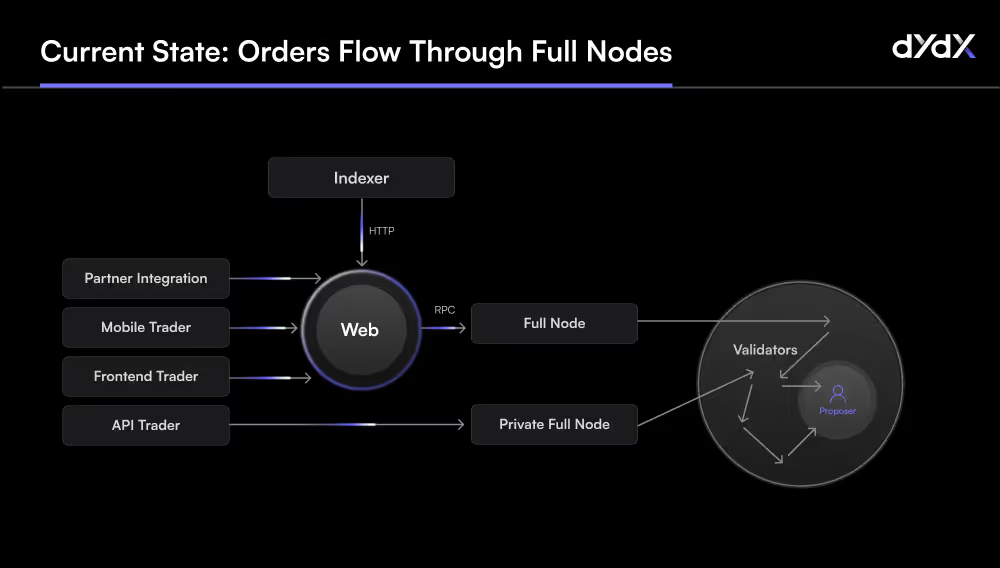

### 1. Previous State

In dYdX previous architecture (original blog post [here](https://www.dydx.xyz/blog/v4-technical-architecture-overview)), orders from traders — whether via the web app, mobile, API, or third-party integration — are submitted to full nodes, which then gossip them across the network until they reach the current block proposer.

* **Pros**: Fully decentralized, no single point of routing.

* **Cons**: Multi-hop gossip introduces latency and unpredictability.

To achieve competitive speeds, professional trading firms have had to typically run their own private full nodes with streaming enabled, directly injecting orders into the gossip layer.

**Previous State** — orders flow through full nodes, then across an unpredictable set

#### Validator and Full Node Roles

Validators drive consensus, maintain an off-chain in-memory order book, gossip transactions across the network, and propose blocks following a weighted round-robin proof of stake model.

Full Nodes run the same protocol software but hold no staking power—they don’t vote or propose. They gossip transactions, process committed blocks, and stream blockchain state to the Indexer—a read-optimized service that powers trading UIs with order book and trade data.

#### Why Professional Traders run Full Nodes

Full-node access has become a performance necessity for high-speed trading — but it also represents a high barrier to entry—technical, financial, and operational.

Running a full node means orders don’t need to traverse geo-distributed public RPCs — you eliminate middle-hop latency by injecting them directly into the gossip network.

Full nodes also enable real-time streaming of L3 order book updates, fills, taker orders, and subaccount changes—via gRPC or WebSocket—supporting highly responsive UI or algorithmic trading logic.

Historically, traders relying solely on the public Indexer have faced reliability and uptime challenges, making self-hosted nodes the only way to guarantee consistent, low-latency market data. Since April 2025, we've made huge [improvements](https://x.com/AntonioMJuliano/status/1924593158165344628) (98%!) to API performance and reliability.

### 2. Designated Proposers

We recently introduced the concept of designated proposers (blog post [here](https://www.dydx.xyz/blog/governance-controlled-path-reliability-and-performance)) — a governance-selected subset of validators responsible for proposing blocks. This change to the open-source software creates a predictable topology, making it possible to route transactions directly to the next proposer instead of broadcasting widely. This is a fully deterministic enhancement to CometBFT that brings increased resilience, network performance, and operational clarity — while preserving the full validator set, stake-based voting power, and decentralized governance of the network.

### 3. The Order Entry Gateway Service (OEGS)

The OEGS builds on the designated proposer model by creating a specialized set of gateway nodes that:

* Peer directly with all designated proposers.

* Accept orders via public, high-performance endpoints (gRPC).

* Bypass standard gossip, broadcasting orders in a single hop to the proposer set.

This infrastructure built to:

* Simplify access – traders can send orders to a public, high-performance gRPC endpoint instead of deploying their own nodes.

* Ensure fairness – the Gateway peers directly with validator nodes, improving routing latency and propagation uniformity.

* Scale gracefully – governance can update, expand, or delegate the Gateway set without disrupting overall network topology.

Gateway nodes streamline communication between traders and proposers, replacing the need for multiple gossip hops with direct and parallel message delivery.

### How It Works: Infrastructure Flow

1. Trader submits an order via UI, API, or third-party partner integration to the OEGS.

2. OEGS full nodes processes validation checks (similar to regular full node).

3. Gateway is persistently peered with the proposer set—gossiping the order directly, bypassing standard gossip hops due to direct peering.

4. Designated proposers include it in the next proposed block by consensus.

5. Order fills are committed on-chain; full nodes and Indexers update their state accordingly.

This streamlined flow ensures minimal latency while preserving decentralization and consensus integrity.

#### Deployment Options

dYdX Labs plans to fully open-source the OEGS code and infrastructure requirements. Any community deployed infrastructure (e.g., front-end, mobile app, API) could consider sending orders to the OEGS but this remains fully opt-in.

Traders may still send orders directly to a full node which maintains decentralization and censorship-resistence. Governance may consider additional incentives for an OEGS operator, given their elevated role and service expectations.

#### For Market Makers & Traders

You’ll get the benefit of ultra-low-latency order routing and immediate streaming data—without the burden of node deployment or uptime management. It levels the playing field between solo operators and well-resourced trading firms.

### Getting Started

Head over to the OEGS endpoints [here](/interaction/endpoints) or take a look at the Node client Python example [here](/interaction/endpoints#node-client).

OEGS complements full-node streaming, validators’ performance, and indexer infrastructure. We’re planning further enhancements to scale alongside trader needs.

:::info

DISCLAIMER

The OEGS Gateway service (the “Service”) is provided and operated solely by Imperator Alliance – FZCO (“Imperator”), an independent third-party service provider. Imperator is entirely independent from, and is not owned or otherwise affiliated with dYdX Operations Services Limited ("DOS”).

DOS does not (i) provide, operate, or make available the Service, (ii) exercise any control over the Service, or (iii) assume or accept any responsibility or liability whatsoever in connection with the Service, including, without limitation, with respect to its availability, functionality, security, accuracy, or reliability. Reference to the Service on any DOS-related website, documentation, or resource does not constitute, and shall not be construed as, an endorsement, recommendation, or guarantee by DOS.

Without limiting the generality of the foregoing, under no circumstances shall DOS be held liable or responsible to any person or entity for any claim, demand, cause of action, damages, losses, liabilities, costs, or expenses of any kind, whether direct, indirect, incidental, punitive, special, consequential, exemplary, or otherwise, arising out of or in connection with: (a) access to, reliance upon, use of, or inability to use the Service; (b) any information or content made available through the Service; or (c) any activities, transactions, or conduct undertaken via the Service.

Access to and use of the Service is undertaken solely at the risk of the user and is subject exclusively to the terms, conditions, policies, and practices established and maintained by Imperator, all of which are independent of, and not reviewed, approved, or enforced by, DOS.

:::

## Intro to dYdX Chain Architecture

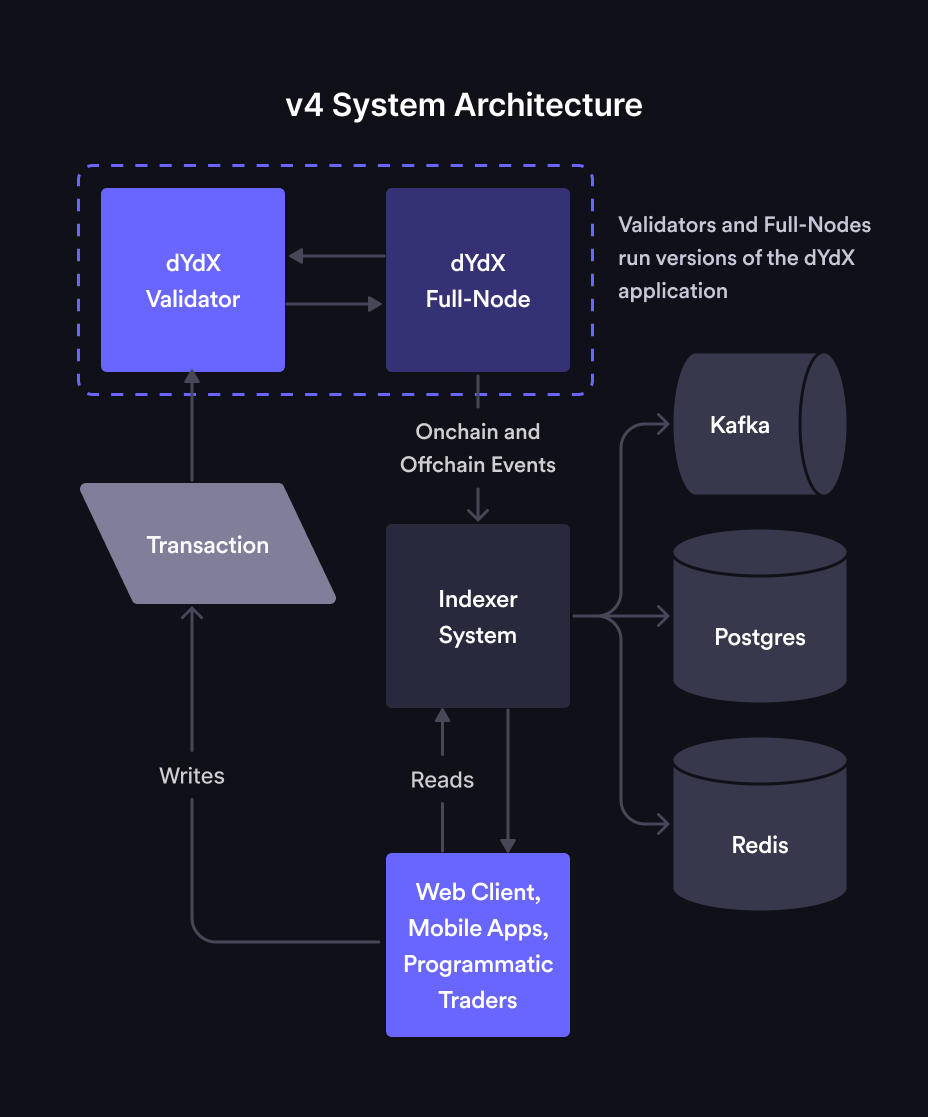

#### System Architecture

dYdX Chain (sometimes referred to as "v4") has been designed to be completely decentralized end-to-end. The main components broadly include the protocol, the Indexer, and the front end. Each of these components are available as open source software. None of the components are run by dYdX Trading Inc.

#### Protocol (or "Application")

The open-source protocol is an L1 blockchain built on top of [CometBFT](https://dydx.exchange/blog/v4-technical-architecture-overview#:~\:text=on%20top%20of-,CometBFT,-and%20using%20CosmosSDK) and using [CosmosSDK](https://docs.cosmos.network/). The node software is written in Go, and compiles to a single binary. Like all CosmosSDK blockchains, dYdX Chain uses a proof-of-stake consensus mechanism.

The protocol is supported by a network of nodes. There are two types of nodes:

* **Validators**: Validators are responsible for storing orders in an in-memory orderbook (i.e. off chain and not committed to consensus), gossipping transactions to other validators, and producing new blocks for dYdX Chain through the consensus process. The consensus process will have validators take turns as the proposer of new blocks in a weighted-round-robin fashion (weighted by the number of tokens staked to their node). The proposer is responsible for proposing the contents of the next block. When an order gets matched, the proposer adds it to their proposed block and initiates a consensus round. If ⅔ or more of the validators (by stake weight) approve of a block, then the block is considered committed and added to the blockchain. Users will submit transactions directly to validators.

* **Full Nodes**: A Full Node represents a process running the dYdX Chain open-source application that does not participate in consensus. It is a node with 0 stake weight and it does not submit proposals or vote on them. However, full nodes are connected to the network of validators, participate in the gossiping of transactions, and also process each new committed block. Full nodes have a complete view of a dYdX Chain and its history, and are intended to support the Indexer. Some parties may decide (either for performance or cost reasons) to run their own full node and/or Indexer.

#### Indexer

The Indexer is a read-only collection of services whose purpose is to index and serve blockchain data to end users in a more efficient and web2-friendly way. This is done by consuming real time data from a dYdX Chain full node, storing it in a database, and serving that data through a WebSocket and REST requests to end-users.

While the dYdX Chain open-source protocol itself is capable of exposing endpoints to service queries about some basic onchain data, those queries tend to be slow as validators and full nodes are not optimized to efficiently handle them. Additionally, an excess of queries to a validator can impair its ability to participate in consensus. For this reason, many Cosmos validators tend to disable these APIs in production. This is why it is important to build and maintain Indexer and full-node software separate from validator software.

Indexers use Postgres databases to store onchain data, Redis for offchain data, and Kafka for consuming and streaming on/offchain data to the various Indexer services.

#### Front-ends

In service of building an end-to-end decentralized experience, dYdX has built three open-source front ends: a web app, an iOS app, and an Android app.

* **Web application**: The website was built using JavaScript and React. The website interacts with the Indexer through an API to get offchain orderbook information and will send trades directly to the chain. dYdX has open sourced the front-end codebase and associated deployment scripts. This allows anyone to easily deploy and access the dYdX front end to/from their own domain/hosting solution via IPFS/Cloudflare gateway.

* **Mobile**: The iOS and Android apps are built in native Swift and Kotlin, respectively. The mobile apps interact with the Indexer in the same way the web application does, and will send trades directly to the chain. The mobile apps have been open sourced as well, allowing anyone to deploy the mobile app to the App Store or Play store. Specifically for the App store, the deployer needs to have a developer account as well as a Bitrise account to go through the app submission process.

#### Order Entry Gateway Service (OEGS) ?

The Order Entry Gateway represents the next step in dYdX’s multi-stage performance evolution and is made possible by the following 2 designs:

1. Designated proposers — A governance-selected subset of validators responsible for proposing blocks. This creates a predictable topology for faster routing (available in v9 software upgrade).

2. Order Entry Gateway Service (OEGS) — open-sourced infrastructure that provides a direct, optimized path from traders to the proposer set, reducing latency, increasing throughput, and lowering barriers for professional and retail traders alike (available now on testnet).

#### Lifecycle of an Order

Now that we have a better understanding of each of the components of dYdX Chain, let's take a look at how it all comes together when placing an order. When an order is placed on dYdX Chain, it follows the flow below:

1. User places a trade on a decentralized front end (e.g., website) or via API

2. The order is routed to a validator. That validator gossips that transaction to other validators and full nodes to update their orderbooks with the new order.

3. The consensus process picks one validator to be the proposer. The selected validator matches the order and adds it to its next proposed block.

4. The proposed block continues through the consensus process.

1. If ⅔ of validator nodes vote to confirm the block, then the block is committed and saved to the onchain databases of all validators and full nodes.

2. If the proposed block does not successfully hit the ⅔ threshold, then the block is rejected.

5. After the block is committed, the updated onchain (and offchain) data is streamed from full nodes to Indexers. The Indexer then makes this data available via API and WebSockets back to the front end and/or any other outside services querying for this data.

## Onboarding FAQs

### Background

1. How does the network work?

* dYdX Chain (or "v4") is composed of full nodes and each maintains an in-memory order book. Anyone can use the open source software to run a full node. Traders can submit order placements and cancellations to full nodes, which gossip the transactions amongst themselves.

* Full nodes with enough delegated layer 1 governance tokens participate in block building as validators. Validators on dYdX Chain take turns proposing blocks of trades every \~1 second. The validator whose turn it is to propose a block at a given height is called the proposer. The proposer uses its mempool orderbook to propose a block of matches, which validators either accept or reject according to CometBFT (Tendermint) consensus.

* All full nodes have visibility into the consensus process and the transactions in the mempool. Another component of dYdX Chain is the indexer software, an application that reads data from full nodes and exposes it via REST / WebSocket APIs for convenience.

2. What is the difference between a full node and a validator?

* A full node does not participate in consensus. It receives data from other full nodes and validators in the network via the gossip protocol. A validator participates in consensus by broadcasting votes signed by each validator’s private keys.

3. What are the benefits of running a full node as a market maker?

* Running a full node will eliminate the latency between placing an order and when the actual order is gossiped throughout the network. Without your own node, your order will need to first be relayed to the nearest geographic node, which will then propagate it throughout the network for you. With your own node, your order will directly be gossiped.

* Additionally, running a full node allows you to use [full node streaming](/nodes/full-node-streaming), a feature that aims to provide real-time, accurate orderbook updates and fills.

* Instructions on setting up a full node can be found [here](/nodes/running-node/setup).

4. What is the current block time?

* The current block time is \~1 second on average.

5. What is an indexer?

* The indexer is a read-only service that consumes real-time data from dYdX Chain to a database for visibility to users. The indexer consumes data from dYdX Chain via a connection to a full node. The full node contains a copy of the blockchain and an in-memory order book. When the full node updates its copy of the blockchain and in-memory order book due to processing transactions, it will also stream these updates to the indexer. The indexer keeps the data in its database synced with the full-node using these updates. This data is made available to users querying through HTTPS REST APIs and streaming via websockets. More info can be found [here](/indexer-client).

### Trading

1. How can I understand how finality works on dYdX Chain?

* When your order fills, a block proposer will propose a block containing the fill (visible to the whole network), and then the block will go through consensus. If the block is valid it will be finalized a couple seconds later (in Cosmos-speak this happens at the “commit” stage of consensus after all validators have voted). At that point, an indexer service will communicate the fill to you.

* It is recommended to post orders with a “Good-Til-Block” of the current block height, and adjusting prices once per block. If the block is published without a match to your order, you know that it is no longer active and did not fill.

2. What are the different order types in dYdX Chain?

* There are two order types: Short-Term orders and stateful orders.

* Short-Term orders are meant for programmatic, low-latency traders that want to place orders with shorter expirations.

* Stateful orders are meant for retail that wants to place orders with longer expirations. These orders exist on chain.

3. How does the orderbook work in dYdX Chain for short-term orders?

* Each validator runs their own in-memory orderbook (also known as mempool), and the set of orders each validator knows about is what order placement transactions are in their mempool.

* User places a trade on a decentralized front end (e.g., website) or via the typescript or python client that places orders directly to a full node or validator API.

* The consensus process picks one validator to be the block proposer. The selected validator will propose their view of the matches in the next proposed block.

* If the matches are valid (orders cross, subaccounts well-collateralized, etc.) and accepted by ⅔+ of validator stake weight (consensus), then the block is committed and those matches are written to state as valid matches.

* After the block is committed, the updated onchain (and offchain) data is streamed from full nodes to Indexers. The Indexer then makes this data available via API and websockets back to the front end and/or any other outside services querying for this data.

* Note: the block proposer’s matches are the canonical matches for the next block assuming their block is accepted by consensus.

* Other validators maintain a list of matches and those matches might differ from the block proposer’s matches, but if they’re not the block proposer those matches will not be proposed in the next block.

* Similarly, the indexer is not the block proposer so its list of matches might be different from the block proposer’s matches, until the network reaches finality.

4. Why should market makers only use short-term orders?

* Short-Term orders are placed and can be immediately matched after they’re added to the mempool, while stateful orders can only be placed and matched after they’re added to a block.